Can I Transfer My Property Taxes When I Downsize in Riverside County?

July 6, 2026

July 6, 2026

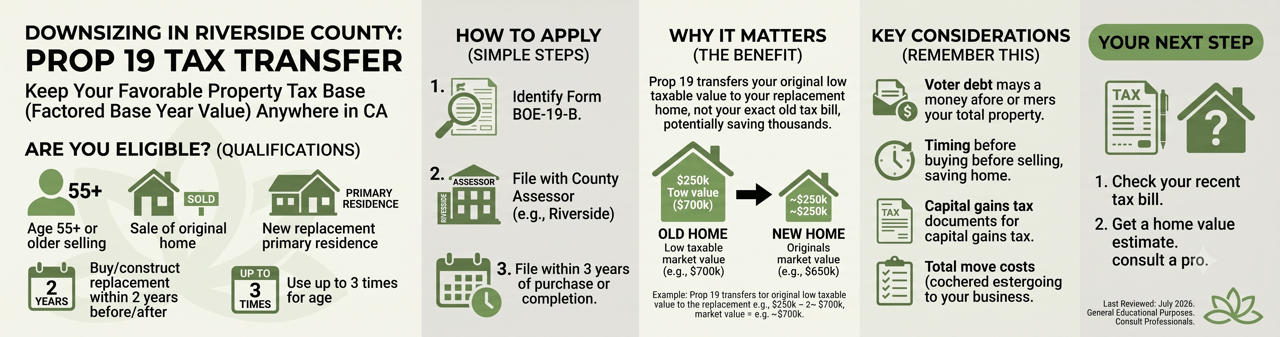

Yes. If you are at least 55 when you sell your original primary residence, Proposition 19 may allow you to transfer its factored base year value to a replacement primary residence anywhere in California. It transfers the taxable value used to calculate property taxes, not your exact tax bill.

Last reviewed: July 2026

Proposition 19 can help eligible homeowners keep some of the property tax benefits they built up while owning a longtime home.

To qualify based on age, the following requirements generally apply:

The replacement home can be located anywhere in California. It does not need to be in Riverside County.

Eligible homeowners who qualify based on age may use this benefit up to three times.

If you are married, only one spouse needs to be at least 55. However, the qualifying spouse generally needs to have an ownership interest in both the original property and the replacement property.

Homeowners who qualify based on age normally use Form BOE-19-B.

The form should be filed with the county assessor where the replacement property is located. If your replacement home is in Riverside County, the claim is filed with the Riverside County Assessor-Clerk-Recorder.

The claim should be filed within three years of purchasing or completing the replacement residence to receive relief from the qualifying transfer date. A late claim may still be approved, but the tax relief generally begins in the calendar year the claim is filed.

Many longtime Riverside County homeowners have a factored base year value that is much lower than their home’s current market value.

For example, someone may own a home worth $700,000 while its taxable value is only $250,000. Without a qualifying transfer, purchasing another home could result in the new property being assessed closer to its current market value.

Proposition 19 may allow the homeowner to carry the $250,000 taxable value to the replacement home, with an adjustment when the new home exceeds the applicable value limit.

This can make downsizing or moving closer to family more manageable. However, it does not guarantee that the new property tax bill will be the same as the old one.

A homeowner sells a Riverside primary residence for $700,000. The home’s factored base year value is $250,000.

Three months later, the homeowner buys another California home for $650,000.

Because the replacement home was purchased within the first year after the sale, it can be worth up to 105 percent of the original home’s full cash value without an adjustment to the transferred value.

The calculation would be:

Since the replacement home is below the $735,000 comparison amount, the homeowner may be able to transfer the full $250,000 factored base year value.

Using the same original property:

The first-year comparison amount is $735,000.

The amount above that limit is:

$800,000 minus $735,000 equals $65,000.

That $65,000 would generally be added to the transferred factored base year value:

$250,000 plus $65,000 equals an estimated new taxable value of $315,000.

The replacement home may therefore receive a taxable value of approximately $315,000 instead of being assessed at the full $800,000 purchase price.

These are simplified examples. The county assessor determines the official full cash values and the final taxable value.

The amount used for comparison depends on when the replacement home is purchased or completed:

You may still buy a home that exceeds these amounts. The difference above the applicable limit is generally added to the taxable value being transferred.

Proposition 19 transfers the factored base year value, not the exact amount of property tax you currently pay.

Your new bill may also include:

These amounts can vary between neighborhoods and properties.

You can purchase the replacement residence before selling your original home, as long as the transactions are completed within the required two-year period.

However, the transfer becomes effective on the latest qualifying date. This may be the sale date of the original home, the purchase date of the replacement home, or the completion date of new construction.

When the replacement home is purchased first, it may initially be taxed based on its full market value until the original home is sold. Taxes paid for that earlier period generally are not refunded.

The transferable amount is normally the home’s factored base year value. This may not always match the assessed value currently shown on a tax bill.

For example, a property may have received a temporary reduction in assessed value because its market value declined. That temporary reduced value is generally not the amount transferred under Proposition 19.

The assessor can confirm the correct factored base year value.

Proposition 19 relates to California property tax assessments. It does not remove, reduce, or determine any federal or California capital gains taxes that may result from selling a home.

A tax professional should review possible capital gains, exclusions, and other tax consequences before the sale.

A lower property tax assessment is only one part of a downsizing decision. It also helps to compare:

Grove Realty can help you estimate your current home’s value and understand how the sale may fit into your overall moving plan.

Marni Jimenez can also help with the real estate side of downsizing, including sale timing, preparing the home, estimating proceeds, and finding a replacement property. Your county assessor and tax professional should confirm the property tax and income tax details.

Find your most recent property tax bill and request a current market value estimate for your home. You can then take those numbers to the county assessor or a qualified tax professional to get a clearer picture of how Proposition 19 may apply to your move.

This article is for general educational purposes and should not be treated as legal, financial, or tax advice.

You’ve got questions and we can’t wait to answer them.