How Much House Can I Afford in Riverside County Right Now?

May 5, 2026

May 5, 2026

Most buyers in Riverside County right now can afford a home by working backward from the monthly payment, not just the purchase price. With Riverside County’s median sale price around the low $600,000s and 30-year mortgage rates recently near the mid-6% range, a comfortable budget depends on your income, debts, down payment, property taxes, insurance, and how much breathing room you want each month.

A good starting point is to keep your total housing payment in a range that still lets you live comfortably.

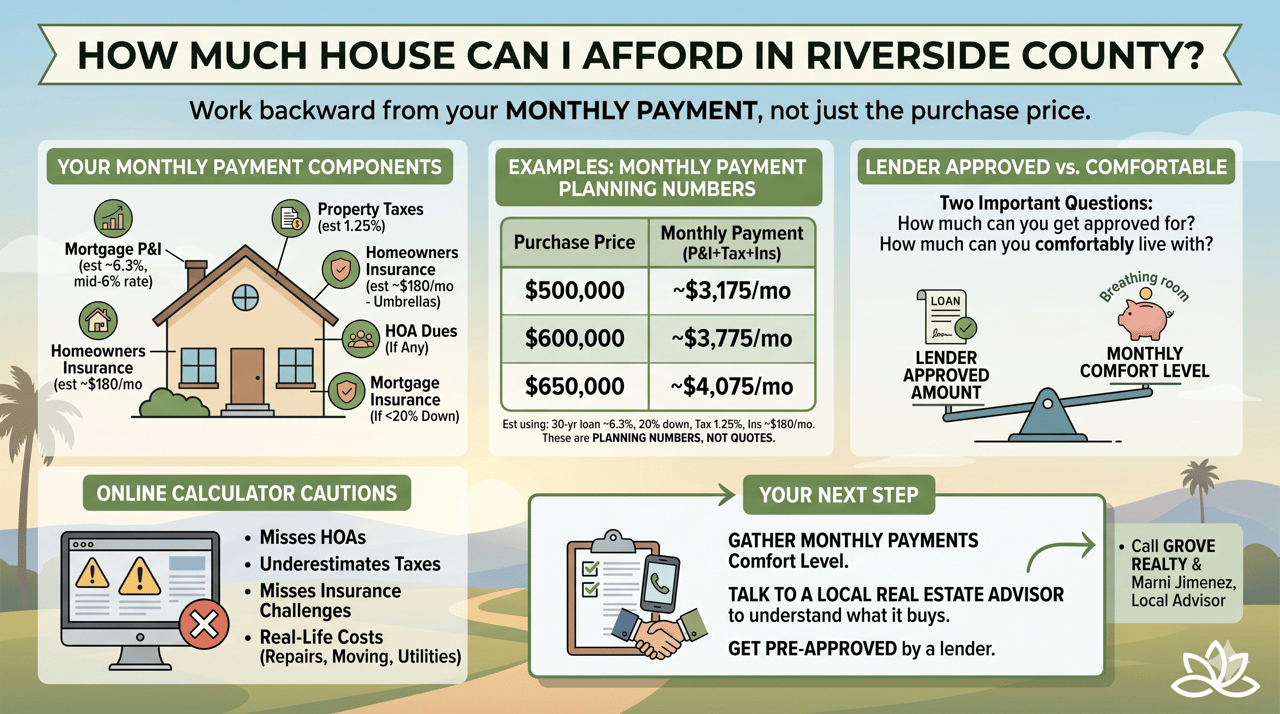

That payment usually includes:

Mortgage principal and interest

Property taxes

Homeowners insurance

HOA dues, if any

Mortgage insurance, if putting less than 20% down

In Riverside County, buyers also need to pay close attention to insurance. Some areas have higher fire risk, and California home insurance costs have been rising, so it is smart to get insurance quotes early, not after you are already in escrow. Riverside homeowners insurance averages vary by source, but recent estimates often land around $1,800 to $2,000 per year for common coverage examples.

The same purchase price can feel very different from one buyer to another.

For example, a $600,000 home may feel manageable for a buyer with a strong income, low debt, and a large down payment. It may feel tight for someone with car payments, credit card debt, student loans, or little cash left after closing.

Also, Riverside County is not one single market. A home in Riverside, Corona, Menifee, Murrieta, Moreno Valley, or the desert communities can come with different price points, tax assessments, HOA costs, commute tradeoffs, and insurance considerations.

That is why “How much can I afford?” is really two questions:

How much will a lender approve me for?

How much can I comfortably live with?

Those are not always the same number.

Here are broad examples using a 30-year loan around 6.3%, 20% down, estimated property taxes around 1.25%, and about $180 per month for homeowners insurance. These are not quotes, just simple planning numbers.

A $500,000 home with 20% down could land around $3,175 per month before utilities and maintenance.

A $600,000 home with 20% down could land around $3,775 per month before utilities and maintenance.

A $650,000 home with 20% down could land around $4,075 per month before utilities and maintenance.

If you put 10% down instead of 20%, the monthly payment will usually be higher because the loan amount is larger and mortgage insurance may apply.

For a simple income check, if you want your housing payment to stay near 36% of gross monthly income, a $3,775 monthly payment would point to about $10,500 per month in gross household income, or about $126,000 per year. Some buyers qualify with a higher debt-to-income ratio, but qualifying is not the same as feeling financially comfortable.

The online calculators are helpful, but they often miss real-life details.

They may not include HOA dues.

They may estimate taxes too low.

They may not reflect current insurance challenges.

They usually do not account for repairs, moving costs, furniture, landscaping, or higher utility bills.

In California, property taxes are commonly discussed as 1%, but the actual bill can be higher once local assessments and voter-approved bonds are included. Riverside County explains Proposition 13 as limiting the general tax rate to 1% of assessed value, plus certain voter-approved indebtedness.

It also helps to remember that the 2026 conforming loan limit for a one-unit home is $832,750, which matters if your loan amount gets close to jumbo-loan territory.

A local lender can give you the cleanest number, but a local real estate advisor can help you understand what that number buys in different Riverside County communities. Grove Realty works with buyers and sellers across Riverside County, and Marni Jimenez can help you think through price, neighborhood fit, resale value, and whether a home really makes sense for your life.

Pick a monthly payment you would feel comfortable with, then ask a trusted local lender to translate that number into a realistic purchase price before you start touring homes.

You’ve got questions and we can’t wait to answer them.