What closing costs should I expect when selling in Riverside County?

April 29, 2026

April 29, 2026

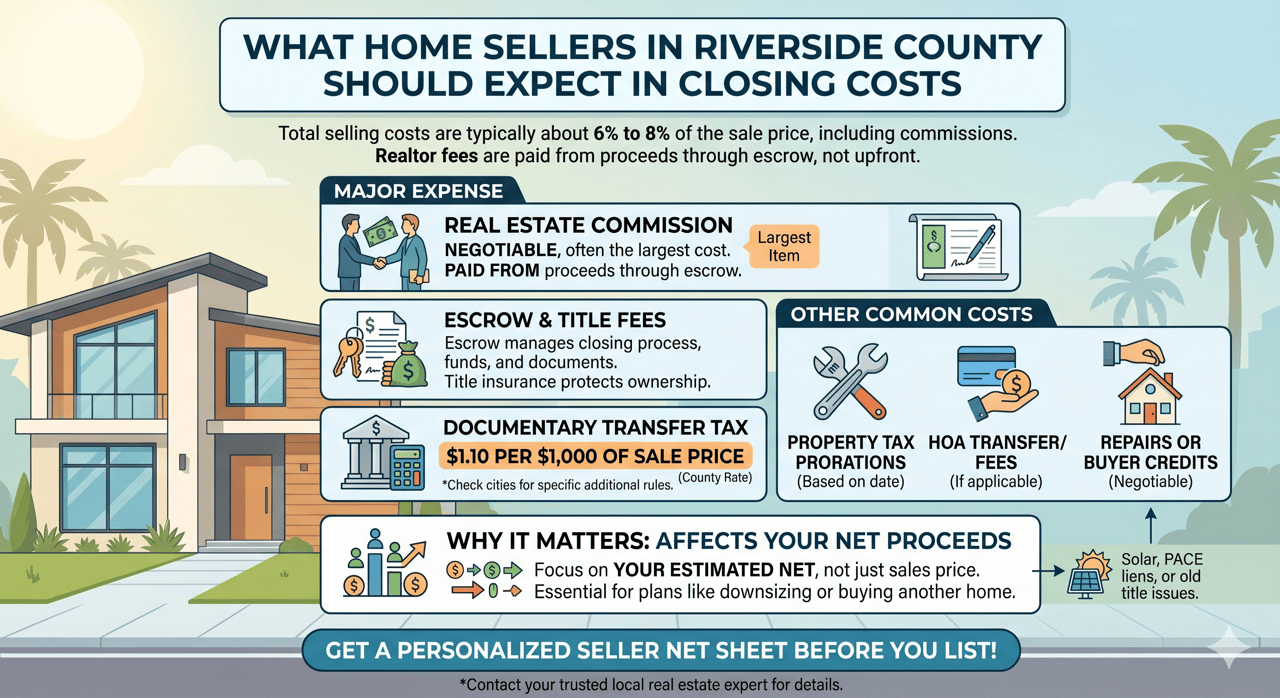

When selling a home in Riverside County, most sellers should plan for about 6% to 8% of the sale price in total selling costs, with the biggest item usually being real estate commissions. Other common costs include escrow fees, title insurance, county and possible city transfer taxes, prorated property taxes, HOA fees, repairs, and any buyer credits negotiated in the contract. Realtor fees are typically paid from the seller’s proceeds at closing, not as an upfront bill.

Seller closing costs in Riverside County are not one single fee. They are a group of costs that get settled through escrow when the sale closes.

The most common seller costs include:

Real estate commission

This is often the largest cost. Commission is negotiable, but it is commonly paid from the seller’s proceeds through escrow.

Escrow and title fees

Escrow manages the money, documents, payoff demands, and closing process. Title insurance helps protect against ownership or title issues. These fees can vary based on sale price, title company, and local custom.

Documentary transfer tax

Riverside County’s documentary transfer tax is generally $1.10 per $1,000 of sale price. Some cities may have their own transfer tax rules, so this should be checked for the specific property address.

Property tax prorations

Property taxes are usually prorated between buyer and seller based on the closing date. Riverside County notes that taxes may be prorated in escrow, but sellers should still review closing paperwork to confirm what was actually paid.

HOA transfer or document fees

If the home is in an HOA, there may be fees for resale documents, transfer processing, demand statements, or account setup. Who pays can depend on the contract and HOA rules.

Repairs or buyer credits

After inspections, a buyer may request repairs, a price reduction, or a credit toward closing costs. This is negotiable and can affect your net proceeds.

Closing costs affect how much money you actually walk away with after the sale.

For example, a seller may focus on the sales price and think, “We sold for $650,000.” But the more useful number is the estimated net after commissions, loan payoff, escrow, title, taxes, repairs, and credits.

This is especially important if you are downsizing, relocating, paying off debt, helping family, or using the proceeds to buy another home. A clear net sheet before listing can help you make better decisions.

A local agent like Marni Jimenez can help estimate these numbers before you go on the market, especially if you are selling in Riverside, Corona, Moreno Valley, Jurupa Valley, Woodcrest, Orangecrest, or nearby areas.

Here is a simple example using a $650,000 Riverside County sale.

A seller might see costs like:

Commission: often the highest cost, depending on the listing agreement

County transfer tax: about $715 at $1.10 per $1,000

Escrow and title: often a few thousand dollars, depending on the company and sale price

Property tax prorations: depends on the close date and whether taxes have already been paid

HOA fees: applies only if the property is in an HOA

Repairs or credits: depends on inspection findings and negotiations

Loan payoff: the remaining mortgage balance, plus any lender payoff fees or interest through closing

Another example: if the home has solar, an HOA, a HERO or PACE lien, unpaid property taxes, or an old lien on title, the final costs may be higher or take more time to sort out.

Not every closing cost is fixed. Some are standard, some are negotiable, and some depend on the buyer’s offer.

A “clean” offer with fewer credits may net you more than a slightly higher offer with large repair requests or seller concessions. That is why it is smart to compare offers by estimated net, not just price.

Also, closing costs are separate from pre-listing expenses. Things like cleaning, painting, repairs, staging, landscaping, inspections, and moving costs may happen before closing, so they should be budgeted too. Grove Realty has seller resources that can help homeowners think through these details before listing.

The most accurate estimate will come from a seller net sheet based on your property, city, estimated sale price, mortgage balance, HOA status, and likely contract terms.

Ask for a seller net sheet before you list, so you can see a realistic estimate of your closing costs and your expected proceeds.

You’ve got questions and we can’t wait to answer them.