How Much Will I Net From Selling My Home in Riverside County?

July 9, 2026

July 9, 2026

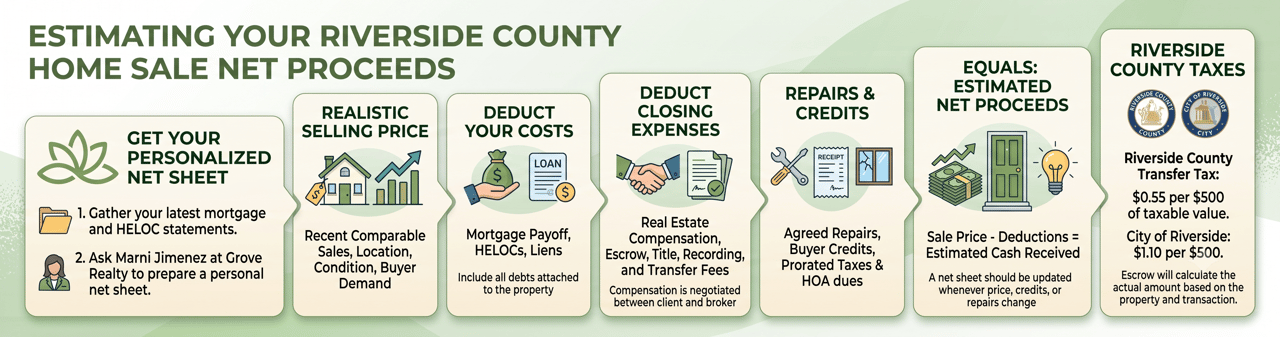

Your net proceeds are the sale price minus your mortgage and other liens, real estate compensation, closing costs, taxes, buyer credits, and any agreed repairs. The most accurate way to estimate what you will receive is to prepare a seller net sheet using a realistic selling price and current loan payoff amounts.

Your home’s selling price and your net proceeds are two different numbers.

A simple estimate looks like this:

Selling price

Minus mortgage, HELOC, and other liens

Minus real estate compensation

Minus escrow, title, recording, and transfer fees

Minus repairs, buyer credits, and prorated expenses

Equals estimated net proceeds

Start with a realistic selling price rather than an online estimate alone. Grove Realty’s guide on what your Riverside County home may be worth explains how recent comparable sales, location, condition, and current buyer demand affect value.

Common seller closing costs may include escrow fees, title insurance, recording fees, transfer taxes, and real estate compensation. Compensation is not fixed by law and may be negotiated between the client and broker.

Riverside County currently lists documentary transfer tax at $0.55 per $500 of taxable value. Property located within the City of Riverside is listed at $1.10 per $500. Escrow will calculate the actual amount based on the property and transaction.

Knowing your estimated net proceeds helps you make decisions before the home goes on the market.

You can use the number to decide:

This is especially important for homeowners who are downsizing. The sale price may sound promising, but the net amount is what determines your real buying power. This Riverside County downsizing guide can help you think through the sale, timing, and replacement home together.

Net proceeds are also different from taxable gain.

Your mortgage payoff reduces the money you receive at closing, but it does not determine your taxable profit. Taxable gain is generally based on the selling price, selling expenses, adjusted cost basis, qualifying improvements, and available tax exclusions.

Eligible homeowners may be able to exclude up to $250,000 of gain from federal income, or up to $500,000 for many married couples filing jointly. Ownership, use, rental history, and previous home sales can affect eligibility, so a tax professional should review your situation.

Consider a homeowner who sells for $650,000.

A general estimate might look like this:

Estimated net proceeds: $395,000

This is only an example. The actual amount will depend on the seller’s contracts, payoff statements, property location, negotiations, and final escrow figures.

Now consider a homeowner who owns the property free and clear. That seller will not have a mortgage payoff, but may still have closing expenses, real estate compensation, transfer taxes, property tax prorations, HOA charges, or buyer credits.

A home with no mortgage does not mean the entire selling price will be received as cash. It simply removes one of the largest deductions.

Another common situation involves inspection negotiations. A seller may begin escrow expecting to net $400,000, but later agree to a $7,500 credit for roofing, plumbing, or another repair. The revised estimate would be closer to $392,500.

This is why a seller net sheet should be updated whenever the price, credits, repairs, or closing terms change.

Your mortgage statement may not show the exact amount required to pay off the loan. Interest, fees, or an early payment charge can make the official payoff slightly different.

Remember to include any HELOCs, solar financing, tax liens, judgments, or other debts attached to the property. These may need to be paid or resolved through escrow.

Property taxes, HOA dues, and certain utilities may also be prorated through the closing date. If the property belongs to an HOA, there may be document, transfer, or account fees.

California real estate withholding can also affect the amount received at closing in some situations. The Franchise Tax Board describes this withholding as a prepayment of income tax, not an additional real estate tax. Exemptions and alternative calculations may be available, depending on the seller and the transaction.

Homeowners age 55 or older who plan to buy another California primary residence may also want to learn about transferring a property tax base under Proposition 19. Grove Realty’s Proposition 19 guide for Riverside County homeowners explains the general rules and questions to ask.

A net sheet is still an estimate. The final settlement statement from escrow will show the actual amount after all credits, payoffs, prorations, and closing charges are entered.

Gather your latest mortgage and HELOC statements, then ask Marni Jimenez at Grove Realty to prepare a personalized seller net sheet based on your home and likely selling price.

You’ve got questions and we can’t wait to answer them.